The WealthChem Learning Lab

The Daily Dose

Every insight we've sent to the free Wealth & Wellbeing Circle on WhatsApp — archived here for anyone who'd rather browse than scroll a chat.

Join the free money-tips community

A free WhatsApp community for simple, no-jargon money tips — no selling, just education. A few short, useful tips a week in the Wealth & Wellbeing Circle on WhatsApp.

Daily Dose posts

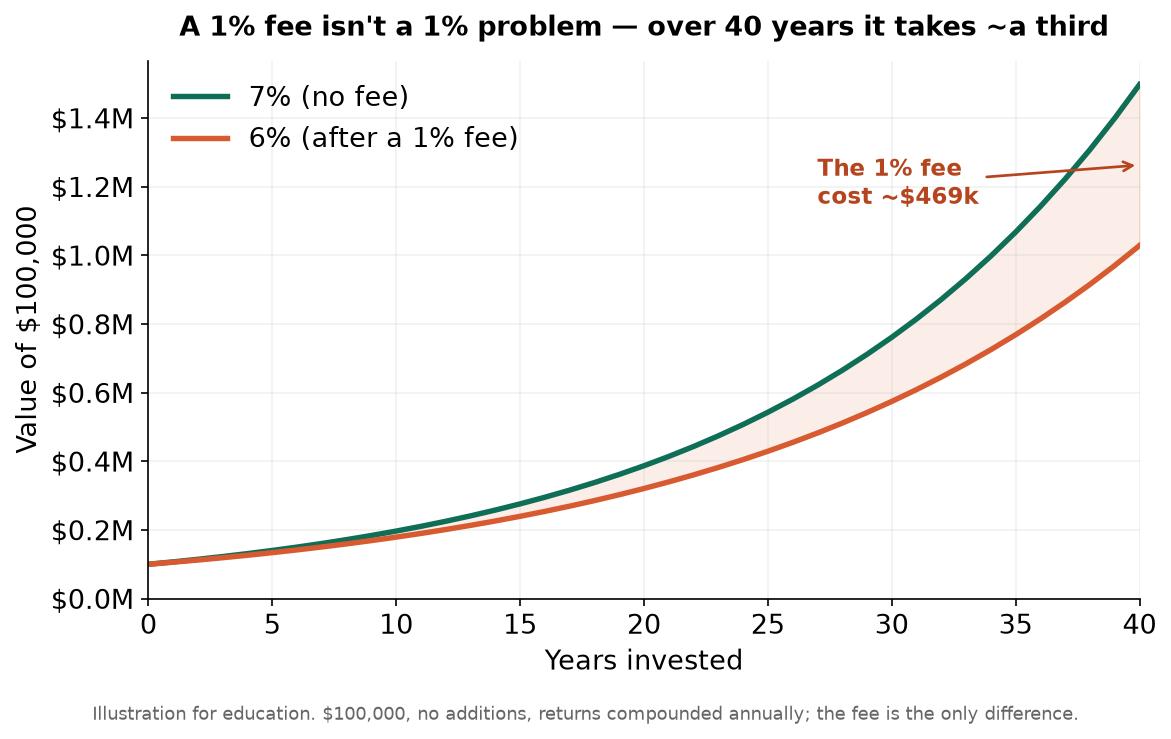

- ChartJul 6, 2026

A "1% fee" doesn't cost you 1% — over 40 years it can cost roughly a third of your money, because the fee compounds away right alongside your gains, every single year. $100,000 growing at 7% reaches about $1.5M in 40 years. At 6% (after a 1% fee) it's about $1.03M instead. That gap — roughly $469,000 — is the fee. Always ask what you're really paying, in dollars, not just percent.

- Account StrategyJul 5, 2026

"Just wait five years" — the Roth rule that's actually two rules, and mixing them up can trigger a 10% penalty. Clock #1 (contributions): your earnings become tax-free once any Roth IRA has been open five years — one clock, starts the January of your first-ever contribution, never resets. Clock #2 (conversions): every traditional-to-Roth conversion starts its own separate five-year timer for penalty-free access to that converted money if you're under 59½. Convert in 2024, 2025 and 2026 and you're running three independent clocks. People assume one Roth means one rule — under current law it's two, on different start dates. (Worth a tax professional's eye before converting.)

- Tax MechanicsJul 5, 2026

Social Security's 2027 raise is tracking high — early estimates put the COLA around 3.8%–4.7% (official figure comes in October). Sounds like pure good news. The catch nobody mentions: the income lines that decide whether your benefits get taxed — $25,000 single, $32,000 married — were written in 1984 and have never been adjusted for inflation. So every COLA nudges more retirees over a line that never moves. A rule meant to hit the wealthiest 10% now taxes roughly half of all beneficiaries. In effect, the raise quietly taxes part of itself back. The lever you control: managing your other income (IRA withdrawals, Roth conversions) to stay under those lines where you can. (SSA / CRS — worth a tax professional's eye.)

- Tax MechanicsJun 17, 2026

If you hold your own employer's stock inside your 401(k), the "automatic" move — rolling everything into an IRA — can quietly cost you. NUA strategy: move the shares in-kind to a taxable brokerage account, pay ordinary income tax only on what you originally paid for them, and the entire appreciation is then taxed at lower long-term capital-gains rates (0/15/20%) — even if sold the next day. Catch: lump-sum distribution only, after separation/59½/disability; once rolled to an IRA the chance is gone for good. (IRS — tax professional's eye.)

- Protection & EstateJun 17, 2026

Your will does not control your 401(k), IRA, or life insurance — a separate beneficiary form does, and it overrides the will. Classic disaster: name spouse, divorce, remarry, update the will, never touch the form → at death the money legally goes to the ex, and no lawyer can undo it. Five-minute lever: confirm primary + contingent beneficiaries on every account/policy.